How to Build Wealth That Can Survive Different Economic Conditions

Most investors worry about inflation, volatile exchange rates, or market volatility.

But the bigger risk that could negatively influence your wealth long-term is over-concentration in one economic system without realizing it.

One question you should be asking yourself constantly as an investor is this:

“If one aspect of the economic system becomes unstable, how protected is my entire networth?”

Because wealth is no longer just about how much money you make.

It is about how well your money is positioned across currencies, markets, asset classes, and geographies against uncertainties.

I recently spoke with an investor I’ll call Faith.

She is financially disciplined, earns well, owns real estate in Abuja, invests in treasury bills, and has built a respectable net worth over the last 8 years.

But during one portfolio review, we noticed something interesting:

Almost everything she owned was connected to the same economic cycle.

Her salary.

Her property income.

Her fixed income investments.

Even her business cash flow.

All tied to one economic environment.

That concentration risk is what many investors ignore.

The goal is not to “run away” from the naira. Nigeria still presents strong local opportunities. The real goal is to avoid building wealth that depends on only one currency, one economy, or one market outcome.

Here’s the framework sophisticated investors are quietly using now.

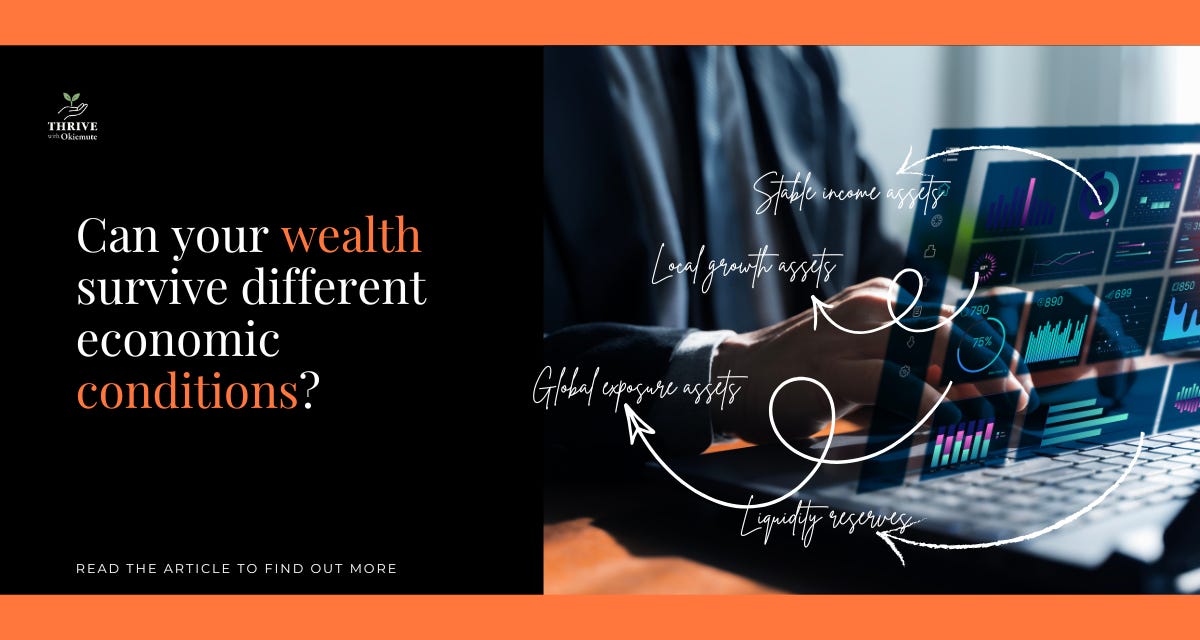

1. Think in Layers, Not Just Investments

Most people focus only on returns.

Smarter investors focus on layers of protection.

Your portfolio should ideally contain:

-

local growth assets,

-

stable income assets,

-

global exposure assets,

-

and liquidity reserves.

Each layer plays a different role.

Your equities may drive aggressive growth.

Your fixed income portfolio may provide stability.

Your global investments may reduce concentration risk.

Your liquid reserves give flexibility during uncertainty.

That structure matters more than chasing the highest return every year.

2. Add Currency Diversification Without Becoming Speculative

Many people misunderstand currency diversification.

It is not about betting emotionally against the naira.

It simply means some parts of your portfolio should have exposure to global currencies and international markets.

This can happen through:

-

dollar-denominated mutual funds,

-

Eurobonds,

-

global equities,

-

offshore ETFs,

-

foreign REITs,

-

international business income,

-

or regulated multi-currency investment platforms.

An investor who owns only naira-based assets is exposed to a single economic engine.

But an investor with both local and international exposure has more flexibility across different market cycles.

That balance is what matters.

3. Build Assets That Earn Beyond Your Geography

One major shift among sophisticated investors is this:

they are prioritizing income streams not fully tied to their physical location.

This could mean:

-

remote consulting income,

-

export-based businesses,

-

digital products,

-

global dividend-paying investments,

-

foreign-currency contracts,

-

or international partnerships.

Why?

Because income diversification is just as important as investment diversification.

A portfolio is stronger when the cash inflow itself comes from multiple economic environments.

4. Don’t Ignore Liquidity Quality

This is one issue many affluent Nigerians underestimate.

An asset is not truly valuable if it cannot be converted efficiently when needed.

Some investors are “asset rich” but structurally illiquid:

-

too much money tied in property,

-

undeveloped land,

-

long-tenor investments,

-

or businesses that cannot easily release cash.

Strong portfolios need a healthy liquidity mix:

-

short-term instruments,

-

medium-term growth assets,

-

and long-term wealth builders.

Liquidity gives you strategic flexibility to leave your investments to breathe and to take advantage of new opportunities.

5. Compliance Is Part of Wealth Preservation

This part is important.

Global investing should always happen through regulated and compliant structures.

Avoid informal FX arrangements, unverified offshore schemes, or unrealistic “guaranteed return” platforms.

Sophisticated investing should be structured, transparent, and sustainable.

I hope this gave you some clarity on building portfolios that are diversified not just across assets — but across opportunities, currencies, markets, and cash flow systems.

If you want help reviewing your current portfolio structure and building a more resilient wealth strategy for today’s market realities, book a private consultation via the link below.